Are you sure you want to perform this action?

Updates

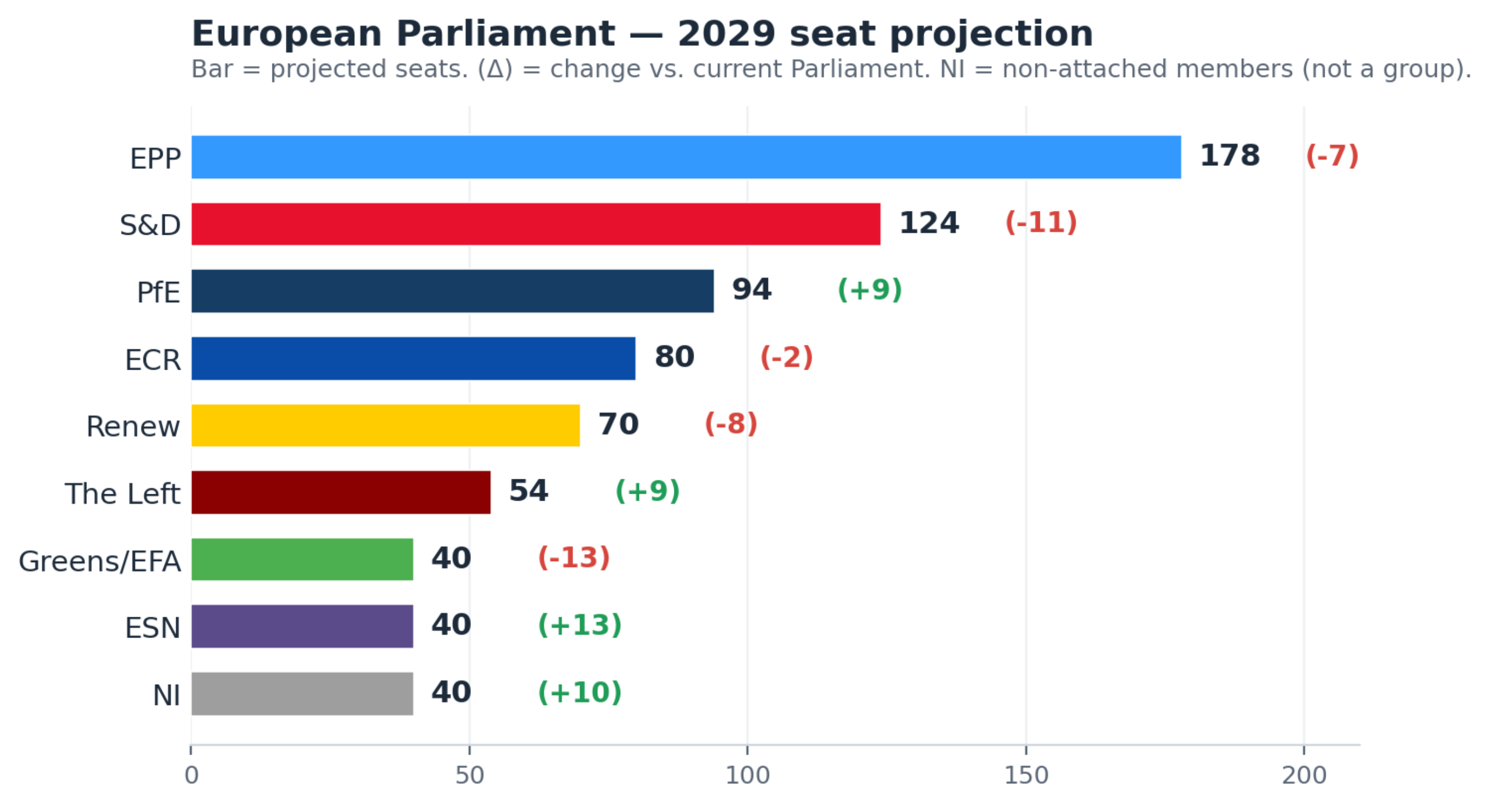

EU '27-'29 Forecast: the political centre keeps shrinking

Two years into the current parliamentary term, the patterns we tracked over previous electoral cycles are holding. Surveys from across the EU point to a slow but steady erosion of the political "mainstream", with the centre of gravity moving further to the right. If the trend holds, the combined forces of EPP, S&D and Renew risk slipping below 50% of seats. The fourth - occasional and reluctant - coalition partner, the Greens, is on course for further substantial losses.

The balance of power in the Council could shift even before the next European elections. Next year will bring a form of European "mid-term": voters go to the polls in France, Italy, Poland and Spain. In each, the hard right stands a realistic chance of entering or retaining government. Meanwhile, in Germany and Romania the governing coalitions are struggling, the hard-right opposition is consolidating its lead, and the likelihood of early elections or a change of coalition is rising.

It is the first time the shift has been this synchronised across so many member states, and it will weigh heavily on policymaking in Brussels. This brief sets out the current trends and what they are likely to mean in the years ahead.

If elections were held this month, the EPP, S&D, Renew and Greens would lose around 40 seats between them. Those seats would pass to the forces opposing the von der Leyen Commission - above all the right-wing fringes (the Patriots and the ESN), but also The Left and left-conservative factions.

DIRECT IMPLICATIONS:

- Individual backbench MEPs gain leverage. Every small defection can prove decisive - and members are well aware of it, and act accordingly.

- The "bridge groups" grow more important - the Greens on the left, the ECR on the right. Paradoxically, the Greens could lose the most seats yet end up with greater influence, should the EPP continue to reach leftward for coalitions, as it does in the overwhelming majority of cases today. The ECR, for its part, becomes difficult to bypass on any major decision or push for regulatory simplification.

- This phenomenon is already under way. Politicians are highly adept at anticipating change, and position themselves so as to capitalise on it.

- Positions are becoming less settled. MEPs are loosening their stances across a broad set of regulatory files as they seek to adapt to - and survive - shifts in public opinion. Some Greens now speaking in defence of farm subsidies is one of many such reversals. Many of the parties gaining ground have not yet had time to develop firm views on much of the regulatory agenda, and will "see as they go".

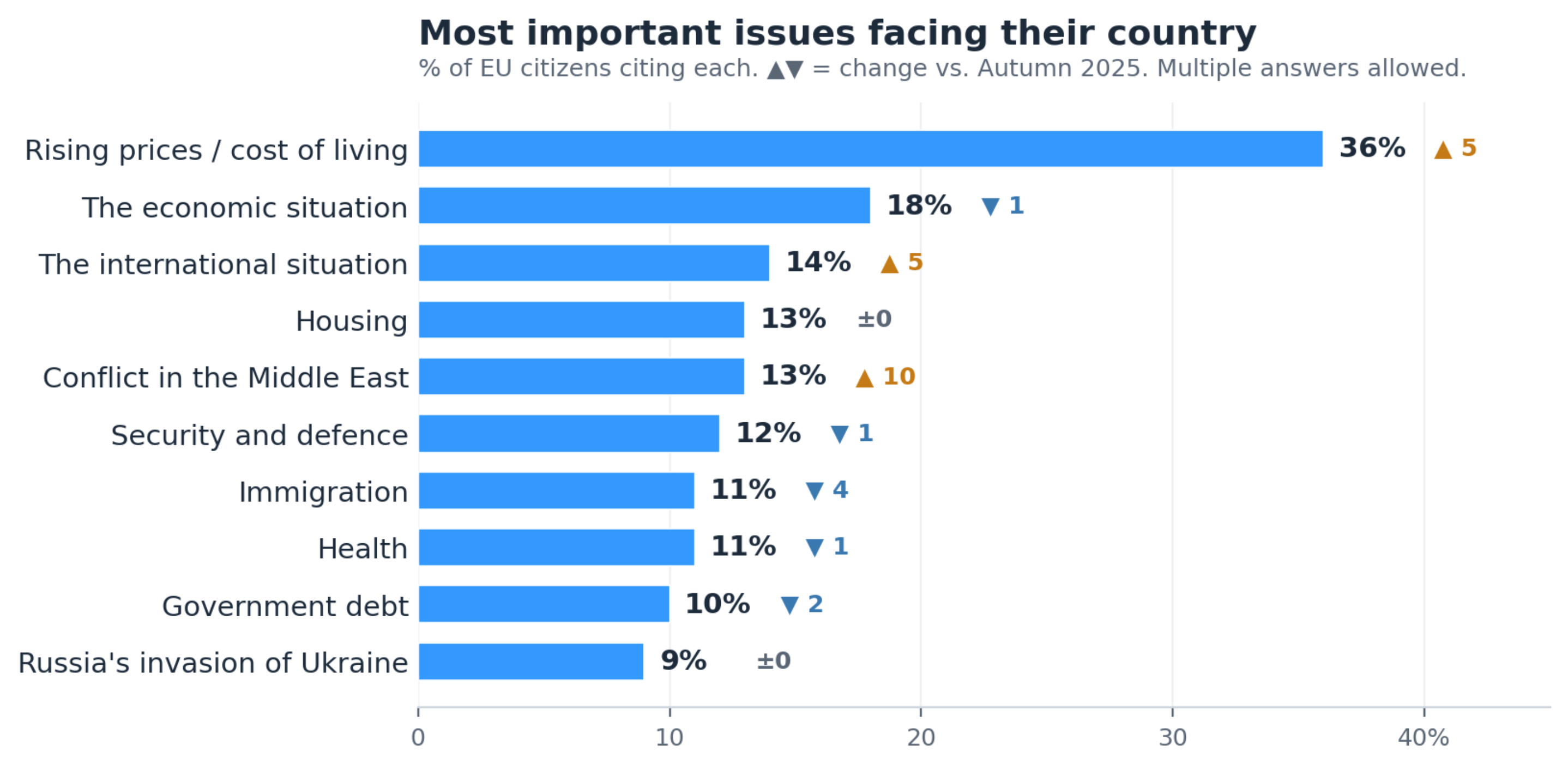

What's driving the discontent: the cost of living sinks leaders fast

Rising prices and the cost of living remain by far the public's foremost concern, according to the latest Eurobarometer. Incumbents are penalised for failing to put the wider economy back on track.

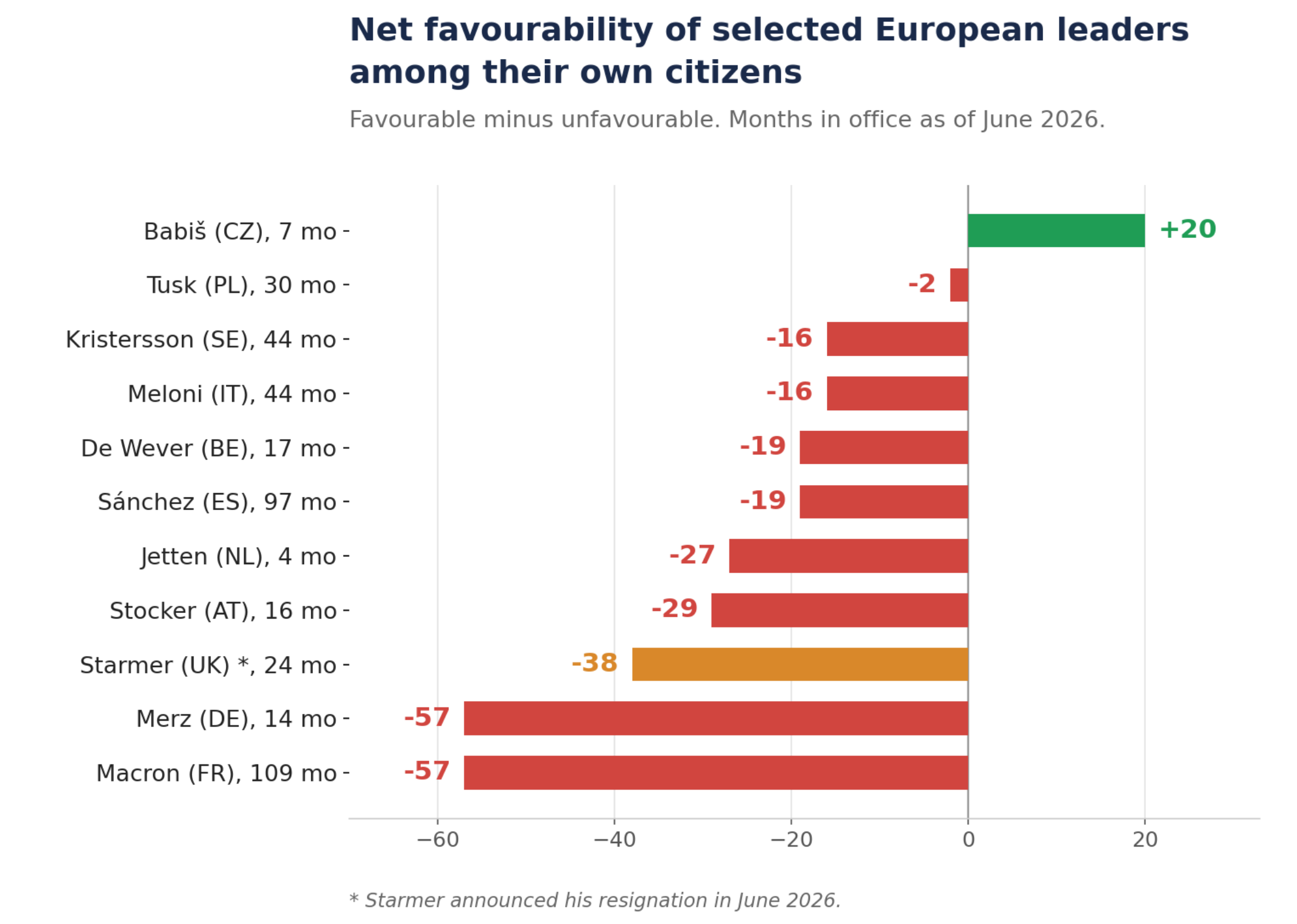

Sitting leaders are bearing the political cost of the wider economic climate. Almost every national leader faces discontent at home, even where the causes lie largely beyond their control. Years of slow growth - especially in Europe - combined with today's higher cost of living have affected governing parties across the democratic world, on both the centre-left and the centre-right, and most acutely in Western Europe's most advanced economies. The strikingly low ratings of leaders of major countries such as Macron and Merz noticeably constrain their ability to lead at the European level.

Time in office shapes the picture. In democratic systems approval naturally erodes, and that is what drives alternation in power: it is no accident that Babiš (seven months in office) is the only leader above water, while the longest-serving, Macron (nine years), sits at the bottom. Yet this decline has accelerated in recent years, with some leaders falling to very low approval levels remarkably quickly - Starmer in the UK, and Germany's chancellors, first Scholz and now Merz. Once popularity erodes, leaders become preoccupied with their own survival, and are tempted to prioritise short-term measures over longer-term strategy.

An early warning sign for governments: net favourability is a reliable signal of governmental stability. The UK's Starmer is a clear example - among the least popular in the set, he announced his resignation in June 2026 despite a comfortable parliamentary majority. Tracking this measure helps professionals anticipate political and policy shifts.

The pivotal moment: the 2027 EU "mid-terms"

Against this backdrop, the hard right is counting on a series of victories that would reshape the EU balance of power before the 2029 elections: a Bardella win in France, a PP-Vox government in Madrid, a PiS return in Poland, another Meloni term in Rome. Were that to occur, the balance in the Council would shift immediately - with consequent effects on alignments in the Parliament and on the pressure exerted on the Commission.

The reverse is equally possible: a broad defeat for nationalists in 2027 would check the right's advance going into 2029. Yet even then, the lesson of the US since 2016 is that diminished momentum does not entail a return to the "comfortably boring" politics of old.

Policy implications

- A blind spot for Brussels. The parties to the right of the EPP remain a "dead angle" for many stakeholders, because coverage concentrates on their positions on cultural and identity questions. Their legislative - and especially their voting - behaviour draws far less scrutiny.

- Their share and positioning counts - not least in the pivot away from stricter environmental targets. As public opinion continues to shift, the "Omnibus-driven" simplification agenda is likely to persist.

- There is no single "hard-right position on regulatory topics". The bloc is far from uniform on regulation - pro-business liberals sit alongside statist and protectionist currents. Determining where each party stands requires a file-by-file, party-by-party analysis to understand what lies ahead.

This is the first in a series we are launching on the upcoming electoral contests and their implications for EU policy. If you would like tailored analysis or a briefing, please get in touch: [email protected]

Sources: eumatrix.eu 2029 projection (June 2026); Eurobarometer 105 (Spring 2026); Morning Consult (April 2026). Figures are projections based on current polling; right-of-centre shares reflect potential support, not agreed coalitions.

Related posts

Categories